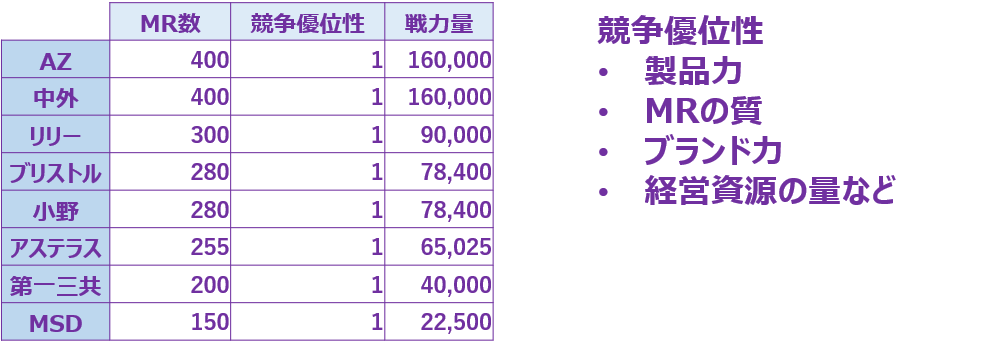

ネット記事で2022年の各社オンコロジー領域MR数の一覧を見つけましたので戦力量を算出してみました(出典不明)。

1位はAZ、次いで中外、リリーの順番です。

各社、製品数や適応症数などが異なるため、一概に比較は出来ませんがMR総数に占める割合も高く、オンコロジー領域に注力していることが窺えます。

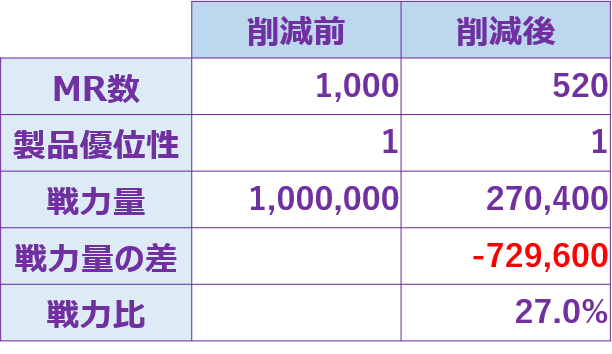

1対1の競争で、競合に圧倒的な差をつけるための戦力差は1:3と言われています。

小野薬品とMSDの戦力量の差がおよそ3倍です。

単純にMRの数による戦力量では、MSDは圧倒的に不利な競争状態です。

MSDがMR数による差を埋めるためには、競争優位性を変数として数値を高めるしかありません。

競争優位性には、製品力、MRの質、ブランド力、経営資源の量などの他に、正確なターゲティングやリソース配分、正しい戦略の選択があります。

MSDはこの数値を4倍にすることで小野薬品の戦力量を上回ることが出来ます。

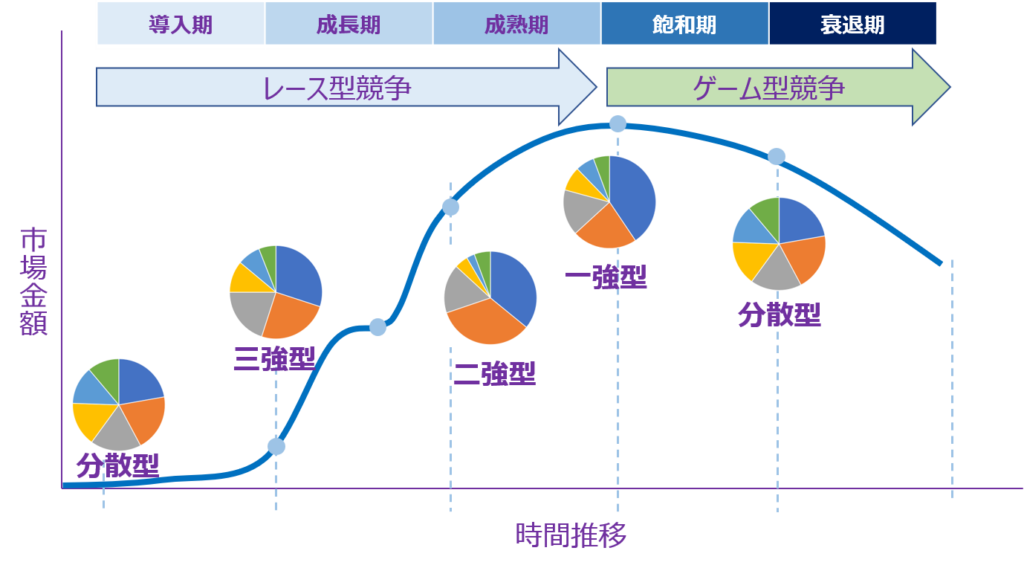

マトリクス分析を用いれば戦略プランニングのデジタル化により定量化および可視化が可能です。

“For MSD to fill the gap in competitive edge”

I found a list of the number of medical representatives (MR) in the oncology field for each company in 2022 through an online article, so I tried calculating the competitive edge.

AZ ranks first, followed by Chugai and Lilly.

Since each company has different numbers of products and indications, it is not possible to make a direct comparison. However, it can be observed that they are focusing on the oncology field as the proportion of MRs is high.

In a one-on-one competition, the competitive edge required to establish a significant advantage over competitors is said to be 1:3.

The difference in competitive edge between Ono Pharmaceutical and MSD is approximately threefold.

In terms of competitive edge based solely on the number of MRs, MSD is at a significant disadvantage in the competitive environment.

The only way for MSD to close the numerical gap is to increase the numerical value with competitive advantage as a variable.

Competitive advantage includes factors such as product strength, quality of MRs, brand power, and the amount of management resources. Additionally, accurate targeting, resource allocation, and selecting the right strategies are also crucial.

By quadrupling this number, MSD can surpass Ono’s strength.

By utilizing matrix analysis, it is possible to quantitatively and visually plan and digitalize strategies.