「MSDが戦力量の差を埋めるには」の続編投稿となります。

小野薬品とMSDのオンコロジー領域MRの戦力量の差においては、圧倒的に小野薬品に優越性があり、MSDはMR数以外の要因を集積して総合的な競争優位性を獲得する必要があります。

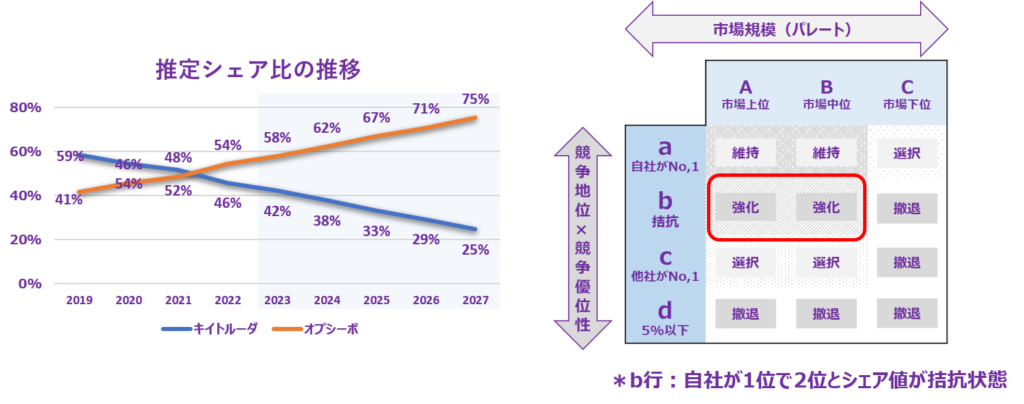

逆に言えば小野薬品は現状の優越性を維持あるいは強化することで、全体市場を占有することが出来るということです。

単純に、シェア比の推移をExcelのTrend関数を用いて試算してみましたが、2027年には2者間競争における勝敗に完全決着がつくことになりました(マーケットシェア理論では市場占有率の目標値は100%ではなく73.9%です)。

「オプジーボ」の国内特許切れは2031年3月になると発表されているので、4年間は圧倒的強者になります(新たな競合製品がない場合)。

マトリクス分析のAb、Bbフレームに分類された施設/顧客にリソースを集中投下して徹底的にMSDを抑え込むことで、さらに早期に決着をつけることが出来るでしょう。

*使用データは施設/顧客の受発注データではなく適応症別データが理想的

受発注データを用いた分析の最大のメリットは自社のみならず競合他社の分析が同時に行えることです。

マトリクス分析による戦略プランは競合の弱点を徹底的に攻める手法です。

受発注データを持つ製薬企業は多いですが、マトリクス分析法と組み合わせれば、競合他社に先手を打ち、反撃される前に勝敗をつけることが出来るはずです。

“How Ono Pharmaceutical can maximize the gap in competitive edge”

This is a follow-up post to “For MSD to fill the gap in competitive edge”

In terms of the gap n competitive edge between Ono Pharmaceutical and MSD in the oncology field’s number of medical representatives (MRs), Ono Pharmaceutical clearly has a superiority, and MSD needs to accumulate factors other than the number of MRs to gain a comprehensive competitive advantage.

Conversely, this means that Ono Pharmaceutical can occupy the entire market by maintaining or strengthening its current superiority.

I tried to calculate the trend of market share using the Excel Trend function, and it turns out that by 2027, the outcome of the competition between the two will be completely settled (according to market share theory, the target market share is not 100% but 73.9%).

The expiration of the domestic patent for “Opdivo” is announced to be in March 2031, so for the next four years, Ono Pharmaceutical will be the overwhelmingly dominant player (assuming no new competing products are introduced).

By concentrating resources on facilities/customers classified in the Ab, Bb matrix frames and thoroughly suppressing MSD, it will be possible to reach a resolution even earlier.

The ideal data to use is indication-specific data, not facility/customer order data.

The greatest advantage of analysis using order data is that it allows you to analyze not only your company but also your competitors at the same time.

A strategic plan based on matrix analysis is a method that thoroughly attacks the weaknesses of competitors.

Many pharmaceutical companies have order data, but by combining it with matrix analysis, they should be able to take the initiative against competing companies and achieve victory before being counterattacked.